滙豐控股(00005)宣布第三輪股份回購計劃,涉及最多20億美元(約156億港元)的股份,預期今年下半年完成。行政總裁歐智華在電話會議中表示,集團今後將以回購作為資本有效管理的其中一種恒常工具,而管理層將每半年檢視一次回購的條件及可能性。

他又表示,滙控暫不會考慮增加派息,今年全年的派息水平將維持在每股0.51美元不變。他強調,回購是資本管理模式,而增加派息與否則視乎盈利前景。

連結

大新推Hello Kitty信用卡搶客

銀行產品部總經理鄧子健表示,申請至年底截止,期望是次推廣活動能令相關理財組合的新客戶達雙位數增長。

鄧子健表示,上半年的銀行新客戶已達雙位數增幅,期望全年增長10%。另外,2017年首季的信用卡消費按年有雙位數增長,略勝市場升幅。

Link Dah Sing

鄧子健表示,上半年的銀行新客戶已達雙位數增幅,期望全年增長10%。另外,2017年首季的信用卡消費按年有雙位數增長,略勝市場升幅。

Link Dah Sing

花旗料中銀香港中期派特息,恒生增季度息

花旗報告表示,2017中期業績料中銀香港(2388)可能在淨息差、貸款增長和利息跑贏同業,料其的過剩資本加上額外資本回報可派0.3-0.5元中期特別息,恒生(11)或將上調季度息至1.2元,而東亞(23)則因較低資本而維持保守派息,或提供較同業為佳的戰略澄清,但或減低併購可能性。

大新金融跌近2%失五十天線,穆迪予港銀行業前景負面

評級機構穆迪發表研究報告指,予香港經濟「Aa2穩定」評級,包括寬鬆貨幣環境、上升

中企業及家庭借貸及物業價格升值,將會影響香港銀行業的信賃狀況,因此穆迪予香港銀行業未來12至18個月「負面」前景展望。

連結

中企業及家庭借貸及物業價格升值,將會影響香港銀行業的信賃狀況,因此穆迪予香港銀行業未來12至18個月「負面」前景展望。

連結

多間大行掉頭減按揭息率

金管局5月「訓導」銀行加按息後,近月銀行故態復萌,整體按息出現趨跌情況,以滙豐銀行為例,貸款額150萬元以上之住宅按揭利率,可低於1個月同業拆息(H)加1.38厘。

不過150萬元以下之貸款利率仍然為H+1.4厘,業界分析,上述做法有助向金管局解釋;此外,中銀香港、恒生銀行、渣打香港亦提供低至H+1.38厘之按揭利率。

連結

不過150萬元以下之貸款利率仍然為H+1.4厘,業界分析,上述做法有助向金管局解釋;此外,中銀香港、恒生銀行、渣打香港亦提供低至H+1.38厘之按揭利率。

連結

重庆银行获批发行5000万境外优先股

证券时报记者获悉,重庆银行境外非公开发行优先股计划已获重庆银监局批准。根据批复,重庆银行获批发行不超过5000万股境外优先股,募集资金不超过人民币50亿元人民币或等值外币,并按照有关规定计入其他一级资本。

去年12月至今,包括哈尔滨银行、邮储银行、招商银行在内的7家银行陆续披露境外优先股发行计划,累计拟发行额达965亿元,其中5家银行在今年3月下旬陆续披露发行计划,累计拟发行额逾800亿元。

http://www.stcn.com/2017/0713/13488856.shtml

去年12月至今,包括哈尔滨银行、邮储银行、招商银行在内的7家银行陆续披露境外优先股发行计划,累计拟发行额达965亿元,其中5家银行在今年3月下旬陆续披露发行计划,累计拟发行额逾800亿元。

http://www.stcn.com/2017/0713/13488856.shtml

匯豐將大新銀行列為首選股

匯豐表示,港銀今年以來已升20%,跑贏恒指和金融股13和14個百分點,雖然淨息差將回升,但市場或低估美國量鬆的過剩流動性需時消退,變相亦高估淨息差回升速度,該行料正常化需時兩年,將行業首選由中銀香港(2388)轉至大新銀行(2356),目標價18.1元,因中銀已反映大量正面因素。

Dah Sing

Dah Sing

Dah Sing Financial should ante up its special dividend to $10

By Man-cheong HUI (translated by KK CHAN and Patrick LEE)

On June 19, Dah Sing Financial (0440) announced the completion of the “Dah Sing-Life “ deal, i.e. the closing sale of its Hong Kong life-insurance business, while having received $8.03 billion as the proceeds of the said deal from the purchaser, Thaihot Investment, a mainland company.

Since then, Dah Sing has called for a directors’ meeting, scheduled to be held on June 26th, for the purpose of duly passing a resolution, concerning the distribution of a special cash dividend of $6.60 per share, as previously proposed.

While it looks set to be cash-rich, even after the special cash dividend distribution has been implemented, and given that a significant price discount-to-NAV would still be evident in the Dah Sing Group of companies' share valuation after the distribution, we hereby urge the board of directors, to either ante up the special cash dividend amount once and for all, or, to make an additional special cash dividend distribution happen immediately thereafter. In this connection, shareholders are strongly advised to proactively voice out their specific concerns, as appropriate.

As I’ve pointed out earlier, while Thaihot Investment has been expected to come up with the required remittance of funds to close the deal without too much of a problem, it’s but a matter of time that the Dah Sing Life deal would then be approved and completed accordingly.

As it turned out, the Hong Kong Dah Sing Life insurance business deal had been completed by mid-June; whereas similar insurance business in Macau, although maybe on a much smaller scale, has yet to be completed. As per Thaihot Investment’s recent press release, however, it is envisioned that the approval from the Macau authorities would be granted soon enough, while Mr. Harold Tsu-Hing Wong, the vice-chairman of Dah Sing Bank, will be participating the signing ceremony.

According to the announcement from Dah Sing Financial, though, the net proceeds after expenses, resulting from the Hong Kong insurance business deal, is about $7.95 billion, while enabling a $3.5 billion pre-tax income.

The use of the proceeds have been outlined, as follows:

1) $2.2 billion will be paid out as a special dividend;

2) $1.45 billion will be used to increase the capital base of the general insurance businesses;

3) $600 million to $1.0 billion will be used to subscribe additional Tier 1 capital to be issued by Dah Sing Bank; and

4) no less than $3.3 billion of the remaining proceeds will be used as general working capital of Dah Sing Financial, and/or for re-investment in its businesses.

As I’ve noted before, too, Dah Sing Financial no longer requires to maintain a huge cash-capital base after the life insurance sale, and as a result, its cash position should be strong enough to distribute a special cash dividend of as much as $20 per share.

In fact, now the use of the proceeds appears to have coincided with the rationale of the aforesaid argument.

For example, out of the approximate $8 billion proceeds, reinvesting in Dah Sing Bank, the crown jewel of the Group, requires just as little as $600 million to $1 billion. On the other hand, as much as $3.3 billion, or as high as $9.85 per share, have been designated for its working capital sourcing. Which means if the same is chosen as a means of distribution, at least $16.45 per share as special cash dividend can materialize.

Yet, whether or not Dah Sing Financial should maintain up to $1.45 billion as cash-on-hand, is debatable.

Here is why.

A review of Dah Sing-Life deal’s announcement would most certainly indicate, that the disposal of Hong Kong and Macau insurance businesses already registered a net asset value that could be worth $3.7 billion, while the net asset value of the remaining general insurance businesses in the Group, would just worth $700 million.

That said, given a saturated insurance market, a decreasing trend in demand for high-profit margin and capital, for it to have their capital base dramatically elevated to twice as much as its NAV, is far from realistic. This is notwithstanding the fact that an increase in capital stands to enhance the probability of a potential merger-and-acquisition (M&A).

A Deutsche Bank report has pointed out, that the recent completion of the Dah Sing Life Hong Kong business deal should help eliminate the risk of the deal falling through, thereby enabling an upbeat outlook. After the special dividend, it says, there remains a lot of excess cash capital at the Dah Sing Financial level, something equivalent to as much as $9.85 per share, or, 15% of equity, as at 2016 second half.

Such a scenario, it says, is able to induce investors looking forward to a higher dividend rewards, in the long run. This has made Deutsche Bank choose Dah Sing Financial and Dah Sing Banking (2356) as their top picks among its Hong Kong bank counterparts. Not to mention, that the valuation is still far from high, given a high propensity for being a long-term M&A target.

JP Morgan also notes that the completion of the insurance sale, in part, is set to render investors a peace of mind, resulting in a positive market sentiment in the short run.

Yet it is quick to point out, that a special dividend of as low as $6.60 per share, is not only far from its plausible forecast of $12.00, but it also means something like 63% of the total proceeds from the deal, resulting in an excess-cash-capital scenario in the part of Dah Sing Financial more severe than expected, triggering a more negative shareholder return forecast (lower than the current 30-50 points projection) outlook than envisaged. A payout ratio exceeding 10% is set to protect the share price from downward momentum, notwithstanding.

These two and other reports show that financial houses are mostly of the opinion that after a special dividend of $6.60, there is still excess cash capital in Dah Sing Financial. The marketplace appears to have reached a consensus on that, too.

After the partial completion of the Dah Sing Life deal, its share price rose only 5% and Dah Sing Banking 1.4% (as at June 27).

Let’s do some simple 'maths'.

Dah Sing Financials holds 74.5% stake of Dah Sing Banking, that is, $51.40 per share. The company’s cash on hand, i.e. $23.70 per share, represents half of it. Hence it is safe to say that there is at least 15% valuation discount, even taking the value of Dah Sing Financial’s other assets and listing status into account

As at the end of 2016, Dah Sing Banking’s capital adequacy ratio is 18.3%, and Tier 1 capital ratio 12.7%. It issued USD 250 million subordinated debt same year. In that respect, it is in a better financial shape than, say, East Asia Bank (23), a bank peer of a larger scale.

The insurance policy distribution agreement signed not long ago should be able to bring forth an additional fee income in the next 15 years. And its liquid assets table is solid. All of this points to one thing. The Group doesn’t need such an ample amount of cash on hand. Instead, they'd need to come up with an answer to the following question: how to manage their capital in a better way?

After all, this, as a longer perspective, would be the essence of the matter.

Godahsing.com has always advocated unfolding the hidden value of the Dah Sing Group. By encouraging dialog and positive feedback, we’ve assisted the shareholders and the public to have a better understanding of the Group’s potentials. So far more than 250 investors signed up, and more than $230,000 donation received (planned to re-donate to non-profits eventually). Those who have agreed to act together would represent a total holding of more than $100 million of Dah Sing Group shares. Besides, our initiatives are gaining endorsements by institutions.

Here is how.

First, we advocate that Dah Sing Financial should distribute special cash dividend as much as they can.

Second, the Group should restructure by way of distributing in specie of Dah Sing Banking and the Bank of Chongqing (1963).

Third, the Group should consider facilitating MDah Sing Financial should ante up its special dividend to $10&A potentials in the mid-term.

While agreeing that a special dividend has improved the trading multiples of Dah Sing Financial and Dah Sing Banking, the recent Deutsche Bank report mentioned above has also asserted that further corporate actions could help unfold more value in both companies.

For example, distributing in specie of the two banks can uplift the trading volume of Dah Sing companies’ shares and align the interest of Dah Sing Banking with Dah Sing Financial, its mother company.

Not to mention, that the remaining insurance business could thus be put up for disposal.

All in all, we are far from satisfied with the amount of the special dividend.

We urge the board of Dah Sing Financial to consider ante up it to at least $9.85 per share.

I will send copies of this article, by mail, to the directors of Dah Sing Financials and the Bank of Tokyo-Mitsubishi UFJ. Shareholders.

As a genuine gesture, please express your much-needed views by fax (25985052), by phone, or by mail. The Group’s registered address: 36th Floor, Everbright Center. Please note that the building has been renamed.

Man-cheong HUI is the founder of Godashing.com. HUI has had holdings in shares of the aforesaid companies. Dah Sing , Library

Elliott增持東亞至8%

向東亞銀行(023)興訟的美資對沖基金Elliott,密密增持東亞股份,據聯交所權益披露顯示,截至本月4日已增持至8%水平,對上一次紀錄為7.12%。

Elliott發言人表示,作為長期股東,相信若東亞在企業治理與整體管理上作出根本和重大改善,有潛力釋放其巨大股東價值。東亞發言人則表示沒有回應。

去年7月Elliott第二度向東亞興訟,指東亞與Criteria及三井住友過往的配股協議,是基於不正當目的訂立,要求撤銷部份剩餘協議。案件7月18日在高等法院開審。

連結

Elliott發言人表示,作為長期股東,相信若東亞在企業治理與整體管理上作出根本和重大改善,有潛力釋放其巨大股東價值。東亞發言人則表示沒有回應。

去年7月Elliott第二度向東亞興訟,指東亞與Criteria及三井住友過往的配股協議,是基於不正當目的訂立,要求撤銷部份剩餘協議。案件7月18日在高等法院開審。

連結

德銀上調大新金融目標價至72元 大新銀行18.5元

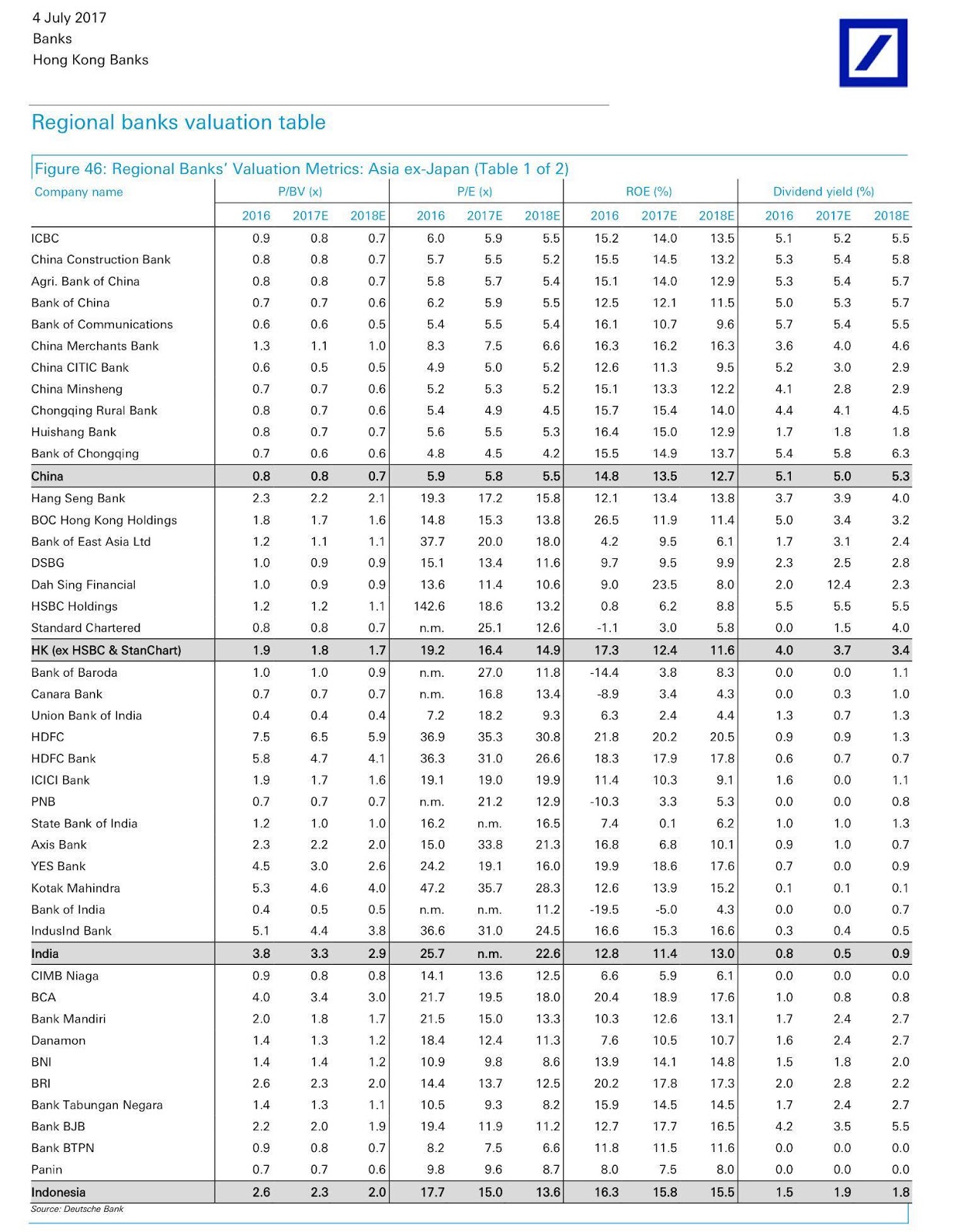

德銀報告表示,加息主題是今年關鍵焦點而營運趨勢至今具支持,但即使港銀收惠加息,盈利改善也是逐步的,惟個別股價特別中銀香港(2388)強勢,只包含正面的不現實期望已反映在股價身上,該股現價已1.6倍市賬率、14倍市盈率和12%預期市盈率,將評級降至「沽售」,維持大新系「買入」評級。

德銀表示,港銀行業現以1.7倍市賬率、15倍市盈率和12倍股東回報率交投,乃較美國大選以來的1.47倍市賬率明顯改善,可見將來加息的好處已反映,而近期中銀香港急升並不合理,大新系估值則仍不高,分別升大新金融和大新銀行(2356)目標價14.2%和8.8%,至72元和18.5元。

德銀認為,在中資銀行遠較大力帶動資產增長之下,港銀的行業狀況已明顯轉變,長遠的主要下行趨勢是貸款增長將被較低利差所抵銷。過去廿年港銀貸存增長2倍和3.5倍,貸存比率也由147%改善至70%,料行業資本較充足和較低的槓桿,已較佳地裝備面對任何挑戰,惟一警告是其與中國更集中和更緊密。

Dah Sing

Dah Sing

德銀表示,港銀行業現以1.7倍市賬率、15倍市盈率和12倍股東回報率交投,乃較美國大選以來的1.47倍市賬率明顯改善,可見將來加息的好處已反映,而近期中銀香港急升並不合理,大新系估值則仍不高,分別升大新金融和大新銀行(2356)目標價14.2%和8.8%,至72元和18.5元。

德銀認為,在中資銀行遠較大力帶動資產增長之下,港銀的行業狀況已明顯轉變,長遠的主要下行趨勢是貸款增長將被較低利差所抵銷。過去廿年港銀貸存增長2倍和3.5倍,貸存比率也由147%改善至70%,料行業資本較充足和較低的槓桿,已較佳地裝備面對任何挑戰,惟一警告是其與中國更集中和更緊密。

訂閱:

意見 (Atom)